Major Exporter Scheme

Find out how the Major Exporter Scheme improves cash flow and reduces tax costs for businesses re-exporting goods, with details on permit requirements and GST suspension.

Last updated 24 February 2026

What Is It?

The Major Exporter Scheme (MES), administered by the Inland Revenue Authority of Singapore (IRAS), helps businesses that re-export a significant portion of their imports by improving cash flow and reducing upfront tax costs.

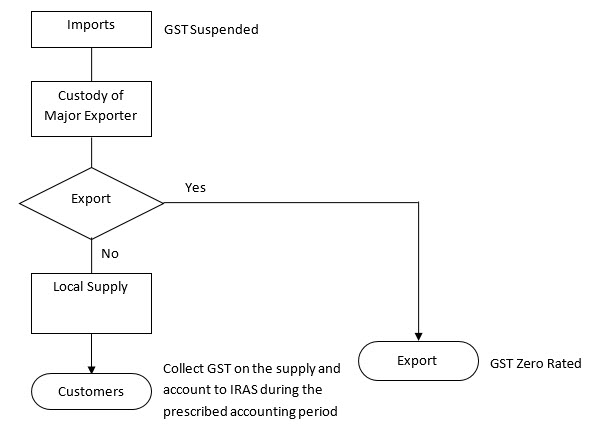

Under standard Goods and Services Tax (GST) rules, you must pay GST on imported goods to Singapore Customs first, before filing your GST return for a refund. For businesses that mainly export goods, this process strains cash flow, as no GST is collected from zero-rated supplies to offset the initial tax paid on imports. The MES removes this barrier.

Once approved under the MES, you can enjoy GST suspension on:

Non-dutiable goods imported into Singapore; and

Goods removed from a Zero-GST warehouse.

This enhances cash flow, operational flexibility, and provides room to grow your export operations.

GST treatment flow for imported goods under the Major Exporter Scheme (MES), showing outcomes for export versus local supply.

Customs Permit Requirements

A Customs In-Non-Payment (Approved Premises/Schemes) permit is required before removing goods from a Free Trade Zone, entry point, or Zero-GST warehouse under the MES. You will need to declare the place of receipt code as “ME”.

A Declaring Agent (DA) can obtain permits only if the MES-approved business has authorised them via IRAS’ online e-Service “Apply for Declaring Agents”.

For postal imports collected at the SingPost Centre, MES traders must present the Customs In-Non-Payment (Approved Premises/Schemes) permit to enjoy GST suspension. Without it, GST must be paid.